Airlines and the end of the business cycle mergers

Airlines and the end of the business cycle mergers

Mergers activity is picking up because too many airlines are not covering their cost of capital, specifically the cost equity, which is an opportunity-cost estimation.

Airlines should not invest in growth when demand is expected to fall next year. The strongest airlines can skillfully navigate their way to increased market share. However, a perilous trajectory unfolds if every airline attempts to maintain its seat capacity share during the denouement of a lengthy business cycle. The weak will shrink or be taken out in a merger, and the merged airline will be smaller than the sum of the two airlines as standalone, at least in the short run. End-of-cycle mergers, analogous to mid-air maneuvers, serve to recalibrate and align the industry for an anticipated economic slowdown.

There is an important balance between investing in growth and providing an adequate return for shareholders. Share repurchases are an important way to compensate shareholders when actual returns are below required (opportunity-cost based) equity returns and the company is throwing off excess free cash flow when the economy is expanding. In other words, airlines should not invest in the airline or growth if they cannot make a compelling case that the potential exists to cover capital costs over a full cycle. If shareholders—the owners of the airline—are not properly compensated, they will withdraw their support, and the market value of equity will fall. If this happens over an extended period, the airline will be forced to cut investment and growth to prop up earnings and cash flow. They must cover operating costs to keep the lights on.

Airlines are in the business of providing adequate returns to the owners of the airline. Providing good service and sustainable growth is necessary for long-term viability, but without adequate shareholder returns, an airline will be forced to restructure or be taken over, akin to choosing between a controlled descent and a hard landing.

Mergers activity is picking up because too many airlines are not covering their cost of capital, specifically the cost equity, which is an opportunity-cost estimation. Repurchasing shares is part of a proper allocation of capital if the returns on growth investment are inadequate or negative, but only if free cash exists and the balance sheet is not over-leveraged. Paying down debt, to achieve an optimal balance sheet mix between book equity and debt, should take priority over share repurchases.

Airlines cannot be blamed for soaring fuel costs, shortages of FAA controllers that cause many of the delays, or the government-mandated pandemic shutdowns that created many of the service issues that have plagued the industry. We've never fully recovered from the government lockdowns that began in 2020. Government policy issues must be considered when evaluating the quality of management.

Many Americans and companies are living on borrowed time because they are increasingly relying on borrowed money. People are spending more than their income growth and are dipping into savings. Since the Great Recession in 2009, we have lived under the Federal Reserve’s financial repression (QE), with below-inflation interest rates and out-of-control government spending. Quantitative tightening (QT) was required to tame the resultant high inflation and to slow economic growth. Higher interest rates now act as headwinds and the sugar high of unsustainable spending will eventually end.

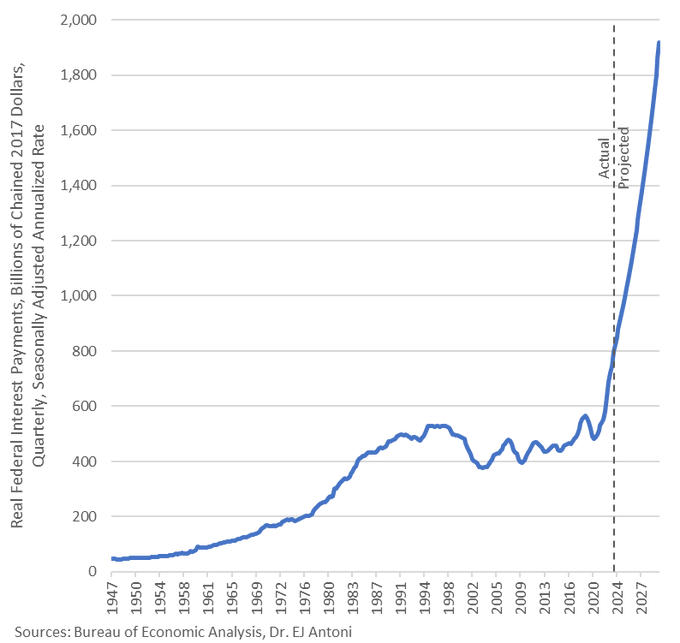

The US has been spending, borrowing, and printing trillions of a year in money for over a decade. Interest on the federal debt is so immense that it’s now consuming 40% of all personal income taxes. The largest source of revenue for the federal government is increasingly being devoted to just servicing the debt, not even paying it down.

Government overspending, overregulating, and printing too much money have come to define the Biden administration and the Democratic Party. This is the record since Joe Biden was elected President. The government has gotten so big and powerful that public policy matters in terms of returns on investment and impact on the broader economy. When the treasury must borrow trillions of dollars to fund massive spending by the government, year after year, it drives the 10-yr rate which impacts borrowing costs across the broader economy. Mortgage rates, car loans, and credit card rates have soared. So, too, has the discount rate employed to value companies and the borrowing costs for businesses, especially over-indebted airlines.

Airlines that lost money over the last several years will be in trouble when economic growth slows or contracts in 2024. Several airlines may not survive over the next decade when long-term economic growth is expected to be below potential. This is due to excessive debt and the need to raise taxes and/or cut social spending. Just as a pilot evaluates and optimizes the payload for a smooth and efficient flight, these airlines must carefully manage their financial “debt payload” and capacity to navigate the challenging economic landscape ahead.