Buckle Up and Hunker Down: A Tactical Approach to Treasury Investments in Uncertain Times

Buckle Up and Hunker Down: A Tactical Approach to Treasury Investments in Uncertain Times

If the market yield on a 10-yr treasury note exceeds 5%, investors can buy the notes at a substantial discount to par and lock in a nice coupon rate. The key is to sell during an economic slowdown.

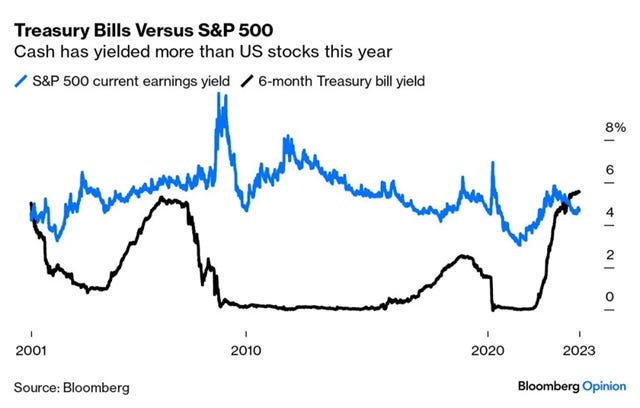

In recent weeks, I purchased 6-month Treasury bills, securing new positions last week with a yield of 5.57%. A yield that currently exceeds the rate of return (earnings yield) for US stocks this year. The strategy is to increase duration by moving out on the yield curve, particularly when the 10-year Treasury market yield surpasses 5%, as it did last Thursday (intraday).

Anticipating a recession in the first half of 2024, the beaten down 10-year notes should rebound nicely in terms of price appreciation. To illustrate, a 1% reduction in the 10-year yield corresponds to approximately a 10% increase in the note's price, alongside the accrual of the coupon rate.

Insight into demand and pricing will be gleaned from the November government auction for 10-year notes. In the next few months, the 10-year yield could fluctuate between 4.5% and 5.5% before potentially declining to as low as 3.5% during the expected recession in 2024. The yield will transition to a higher “new normal” as the economy recovers. The time to sell the 10-yr is during the recession and after the note has appreciated in value.

The new higher longer-term rates will reflect the issuance of massive amounts of debt by the US government. This is required to finance over $20 trillion in new deficit spending over the next 10 years. Hence, a great reason not to hold long dated U.S. Treasuries to maturity.

The investment thesis hinges on realizing the base case scenario, potentially yielding a total return of 10-14% over the next 12-18 months. The critical aspect lies in acquiring the 10-year Treasury note at or near the peak in 10-year market yields and subsequently divesting it during the projected slowdown in 2024.

Considering the WSJ (October) consensus of over 70 economists and my estimations regarding the price appreciation of the 10-year note in the next couple of years, let's delve into the fundamental calculations for acquiring a specific 10-year note in the secondary market:

This note has a maturity date of 11/15/2032 with an (ask) price of 94.25 (Oct 20). The yield to maturity (ask) is 4.93%. It has a coupon rate of 4.125%.

The total return math: Annual coupon of 4.125% + 10% price appreciation = 14%.

The paramount question revolves around the timing – when to buy and when to sell.

Total return estimates for various maturities based on change in yields is highlighted by the following graph.

It’s noteworthy that analysts and economists exhibit substantial variability in their forecasts, and collectively they have often erred in predicting aspects such as inflation, GDP, interest rates, consumer spending, job growth, and other pivotal metrics since the pandemic lockdown. Hence, it is prudent to regard the consensus with a high degree of skepticism. It is the investors and business executives with financial exposure who tend to offer more accurate forecasts.

The recent Conference Board report highlights the reasons it expects a recession in 2024. See below. Economists have reduced the likelihood of a recession within the next year from an average of 54% in July to a more hopeful 48%. This is the first drop below 50% since the middle of last year. As a contrast, 84% of CEOs see a looming recession, which is based on The Conference Board’s CEO survey. I’ll go with the CEO’s forecast. Economists, especially academic and government, have a long history of lousy forecasting.

If the market yield exceeds 5%, investors can buy 10-year notes at a substantial discount to par value. This is a tactical maneuver, not intended for holding until maturity but for selling during the economic slowdown expected in 2024. This slowdown is largely attributed to the spike in the Fed Funds rate and for the Treasuries (notes and bonds) at the long end of the yield curve.

The continued tightening of financial cycle conditions with lower inflation and poor economic performance will mean that long dated U.S. Treasury yields will trend lower.

These upcoming quarters may entail significant challenges, both economically and in the financial markets. Positioning the portfolio to align with the impending circumstances is vital for preserving capital, particularly in an era characterized by war, chaos, inflation, deficit-spending, and unsustainable debt, which is exemplified in the Biden era.

Good luck,

Vaughn

The Conference Board’s latest Economic Outlook report.

The US economy will likely tip into a short and mild recession in 2024

The Conference Board forecasts that economic weakness will intensify and spread more widely throughout the US economy over the coming months, leading to a short and mild recession in the first half of 2024. Consumer spending is expected to worsen as households grapple with slower income growth, mounting debt, dwindling savings, and other headwinds. The US labor market remains tight, but there are some signs that labor demand is cooling. Job openings are moderating, and the labor force participation rate is rising, both of which will push the unemployment rate higher. On inflation, progress is being made, but more work remains to be done. We expect the Federal Reserve to raise rates one more time and keep rates steady until around mid-2024. This backdrop suggests real GDP growth will decelerate from 2.2 percent in 2023 to just 0.8 percent in 2024, including two quarters of negative GDP growth in Q1 and Q2.