McDonald's: Fat Profits for Shareholders

McDonald's dominates the fast food industry, holding a 43% share of the market capitalization in the industry. The company generates significant free cash flow and 33% net profit margins.

At Golden Arches, Vaughn's delight, Big Macs and fries, his favorite bite. Quick with numbers, always right, Loves the taste, but fears weight's plight. Fast food sales ascend, oh, they fly, Shareholders' profits, multiply high! Those with less, at home they fry, Inflation's toll, in weight and dime, oh sigh!

Inflation in the fast food sector has resulted in substantial profits for McDonald's and its shareholders.

A recent study by FinanceBuzz revealed that fast food prices have escalated more rapidly than inflation since 2014, with McDonald's experiencing the highest increase.

Driven by curiosity and a fondness for Big Macs, I examined 30 years of McDonald's financial records to understand the effects of fast food inflation on shareholder returns.

Since 2014, McDonald's food prices have seen a 100% increase, aligning with a 92% expansion in profit margins.

Concurrently, the company's market cap has risen by 114%, and its share price has surged by 176% as of April 15, 2024.

The Bureau of Labor Statistics reports a 31% increase in the cost of goods since 2014, equating $100 from 2014 to $131 in 2024. A significant portion of this inflation, 22%, occurred in the past five years. Restaurants, on average, have increased their prices by 60% between 2014 and 2024, outpacing the national inflation rate by nearly two-fold.

Fast food chains are often considered to be more resistant to recessions. This is because these restaurants offer affordable meals, which can be attractive to consumers during economic downturns when they are looking to save money.

An analysis of 17 fast food restaurants highlights the strength of McDonald’s (MCD) business model.

McDonald's is a behemoth in the fast food industry, commanding a 43.8% share of the market capitalization. It boasts robust free cash flow and substantial profit margins, with operating margins at 45.68% and net margins at 33.22%. The Return on Invested Capital (ROIC) is 20%, which is the second-highest among the restaurants analyzed.

The company provides a 2.51% dividend yield and is projected to deliver a 24% total return over the forthcoming year. Nevertheless, an intrinsic valuation indicates that the stock's consensus target price may be overestimated by more than 20%.

According to the one-year price targets provided by 38 analysts, the average target price for McDonald's Corp is $325.05, with a high estimate of $357.00 and a low estimate of $299.00. The consensus average target suggests a potential upside of +22.09% from the current price of $266.23. Nevertheless, it is advisable to approach these estimates cautiously, as they tend to be overestimated by around 8%, especially considering the elevated 10-year treasury note discount rate, which diminishes future earnings per share.

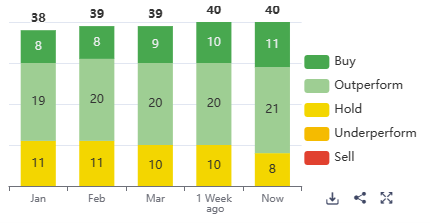

What the analysts say.

The average brokerage recommendation for McDonald's Corp (MCD), derived from 38 brokerage firms, is currently 2.1. This suggests an "Outperform" rating. The scale used for this rating ranges from 1, indicating a Strong Buy, to 5, which signifies a Sell.

The consensus 12-month target prices for the stock range from a high of $377 to a low of $299, with an average of $325. The current price stands at $265.7 as of April 16, 2024, 1:55 pm. Considering the fundamentals and the rising 10-year treasury yield, which serves as the discount rate for valuing future earnings and cash flows, the 'fair' price is likely to be significantly lower than the consensus estimates.

As of the last earnings report, revenue of $6,406M (+8.1% Y/Y) was $47M below consensus. Adj-operating income grew 13.8% Y/Y to $2,940M vs. the $2,916M consensus, with margin at 45.9%.

Same-store sales rose by 3.4% compared to the anticipated 4.6%, mainly due to increased pricing in the high single digits. This was attributed to McDonald's (MCD) difficulties arising from the conflict in the Middle East and decreased expenditure by lower-income consumers, as home dining has become more economical. Moreover, following MCD's ownership increase in China from 20% to 48%, heightened price competition and muted consumer sentiment were noted.

Despite investor optimism about MCD's dedication to affordability and market share expansion in 2024, these recent challenges are expected to continue, considering MCD's restricted capacity to modify pricing and expenses.

What the bull’s say:

“Following a $9 billion investment in remodeling, McDonald's has modernized its restaurant real estate footprint, positioning it to capitalize on the changing digital ordering trends.”

What the bear’s say:

“Wage inflation in the U.S. may lead to heightened price competition, further investments in automation, and a trend towards more affordable substitutes within the food-at-home sector.”

A few statistics to consider.

Growth Rates have been exceptional over the last 12 months:

Analyst estimates (Q/Q:

Analyst estimates (Y/Y:

A Big Mac meal is hard to stop. Paired with fries and a drink of your choice, It's a meal that makes the heart rejoice. But let's not forget, the Big Mac's fame, Is not just in its taste, but also its name. For in the world of burgers, it's a classic, a star, The Big Mac, from McDonald's, you've raised the bar.