The wealth effect in reverse: when real estate and the stock market decline

The wealth effect in reverse: when real estate and the stock market decline

Inflated asset values are unhinged from fundamentals because of easy money. If interest rates remain higher than the last 15 years, asset values will need to be repriced.

Consumers and businesses are currently in a strong position, and most economists believe there will not be a recession this year. Geopolitical risk is high, and oil and gasoline prices are soaring. Inflationary pressures persist, and the full impact of the Fed’s quantitative tightening policies has yet to be felt.

If interest rates remain at current levels or go higher, or if economists’ forecasts prove incorrect, real estate and stock market values could decline significantly. This could lead to a reverse wealth effect, causing consumers to slow their spending as asset values fall. As a result, economic growth may slow, and corporate earnings could decline. The worst-case scenario is stagflation.

The wealth effect

The wealth effect is a behavioral economic theory suggesting that people spend more as the value of their assets rises. The idea is that consumers feel more financially secure and confident about their wealth when their homes or investment portfolios increase in value. This sense of increased wealth makes consumers feel richer, even if their income and fixed costs remain unchanged.

The wealth effect captures the psychological impact that rising asset values, such as those seen during a bull market, have on consumer spending behavior. The theory emphasizes how feelings of security, known as consumer confidence, are bolstered by significant increases in the value of investment portfolios. This heightened confidence leads to higher levels of spending and lower levels of saving.

The theory can also apply to businesses. Companies tend to increase their hiring and capital expenditures in response to rising asset values, mirroring the consumer side.

This means that economic growth should strengthen during bull markets and weaken in bear markets.

The housing market has become “unhinged from fundamentals.”

Lagging wage growth—inflation-adjusted wages are lower than they were three years ago—has meant that homebuyers need to earn about 80% more than they did before the pandemic, Zillow recently found. Fitch Ratings estimates that homes were overvalued by 11% as of the third quarter of 2023, a trend that extends to 90% of U.S. metro areas. Prices continued rising into the fourth quarter due to tight home supplies, and Fitch expects overvaluation to have persisted through the end of last year.

Average mortgage rates remain more than double what they were in 2020 and 2021. The Federal Reserve Bank of Dallas has noted that the housing market has become “unhinged from fundamentals” such as disposable income, the cost of credit and access to it, and rising labor and raw construction material costs. According to the National Association of Realtors, the national median existing-home price is roughly 48% higher than in January 2020.

“The housing market is likely to continue to face the dual affordability constraints of high home prices and elevated interest rates in 2024,” said Doug Duncan, senior vice president and chief economist at Fannie Mae, in an emailed statement. “Hotter-than-expected inflation data and strong payroll numbers are likely to apply more upward pressure to mortgage rates this year than we’d previously forecast.”

With fewer homes selling, Dan Hnatkovskyy, CEO of NewHomesMate, a marketplace for new construction homes, sees a price collapse as a possibility, especially in markets where real estate investors scooped up numerous properties. “If something pushes that over the edge, the consequences could be severe,” said Hnatkovskyy.

Financial analyst Meredith Whitney, renowned for predicting the 2008 financial crisis, declared a “silver tsunami” set to hit in 2024. She anticipates a significant shift, unlocking a massive $18 trillion in housing wealth.

Whitney projects that over 30 million housing units will flood the market as 51% of individuals aged 50 and above downsize to smaller homes, challenging the existing supply-demand dynamic. Whitney emphasizes that this downsizing trend will be “rate agnostic,” unaffected by current market rates due to older individuals often having lower mortgages or none at all.

Chief Economist Mark Fleming from First American provides a counterpoint, asserting that the mass downsizing won’t happen overnight. He notes that baby boomers, who are healthier and wealthier, tend to stay in their homes longer.

The stock market is also unhinged from fundamentals.

Historically, the stock market’s value has been approximately equal to one times GDP, while it is currently 1.84 times the last reported GDP. This suggests a bubble based on fundamentals.

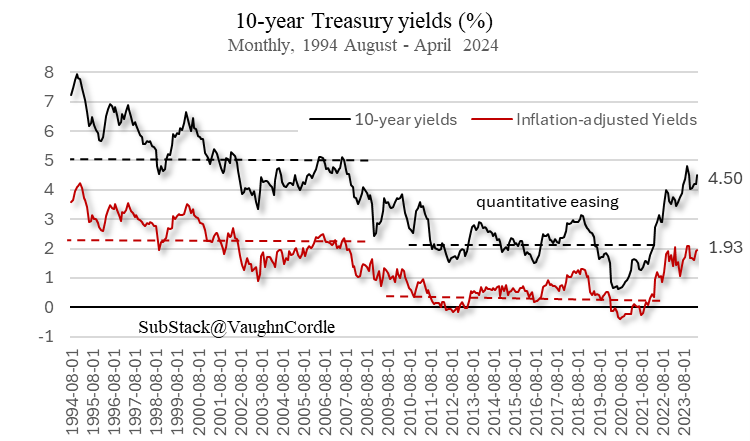

These fundamentals include valuation metrics such as price-to-sales (P/S), price-to-earnings (P/E), and price-to-cash flows (P/FCF), all of which are at unsustainable levels, particularly with 10-year yields currently in the 4.5% range.

The consensus of 73 economists (April 14, 2024, WSJ Survey) expects this rate to decline to 3.78% by December 31, 2026. However, this expected rate could be too low given higher than expected inflation and deficit spending that must be financed over the next ten years.

10-year yields averaged 2% between the years of 2010 and 2022 due to the Fed’s quantitative easing. It averaged 5% over the years between 1994 and 2010. A more normal rate of interest.

A forward P/E ratio of over 21 times earnings is currently too high by roughly 17%. The current P/E is above the 5-year average (19) and above the 10-year average (17.7). Interest rates have been abnormally low because of Federal Reserve monetary policy.

The real (inflation-adjusted) 10-year yield averaged .41% during the financial repression period and averaged 2.29% in the years prior to the Fed’s policy of easy money.

The easy money days are over.

A normalized P/E should be about 16-19 times earnings as the market adjusts to the higher average interest rates expected on the 10-year Treasury. There is an inverse relationship between this key discount rate and the P/E ratio; the higher the discount rate, the lower the P/E. Since 2009, the market has been anchored to below-normal rates, a function of Federal Reserve quantitative easing.

There are two inputs to the P/E ratio: the price of the stock market and its earnings. As the P/E contracts to a more normal range, the market capitalization of the indexes will decrease. Earnings may also start to decline as GDP growth contracts in the second half of this year.

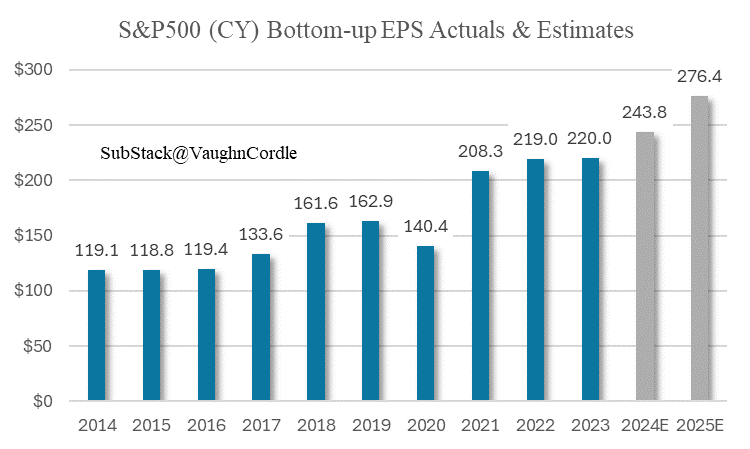

Consensus EPS growth is expected to increase 11% in 2024 and 13% in 2025. This seems too high given the lower real GDP growth expected in the second half of 2024.

The expected average GDP growth of 1.41% (Q2+Q3) is 44% lower than the 2.5% estimated growth in 2023. How can corporate earnings increase in the second half when GDP contracts over 40%? Almost 70% of GDP is consumer spending and if consumer expenditures fall, so will earnings and share prices.

Wall Street is paid to be bullish.

Historically, sell-side analysts have overestimated the closing price of the S&P500 index by 5%-12% over the last 30 years. This is especially true at the end of long economic expansions. However, they did underestimate the year-ahead index close in early March of 2023 when the bottom-up target price was 4,635. By late March in 2024, the index closed at 5,224—11% higher. The excess liquidity from government spending and the wealth effect in action.

If the economy slows as many economists now expect; earnings could fall by 10% or more as the year progresses. The expectation is that (inflation-adjusted) GDP growth slows to 1.7% in 2024—28% lower than 2023’s growth.

If EPS estimates for 2024 are reduced (-10%) to $219 from the current $244, and the P/E contracts to say, 18 times, this suggests an S&P500 index price of 3,900—23% lower than the closing price of 5,123 on April 12, 2024. Of course, these numbers must be taken with a healthy grain of salt because the market discounts more than one year’s worth of earnings into the future. Analysts are constantly revising EPS growth as new information is presented in the quarterly reports. Analysts revise their estimates, in large measure, based on management guidance.

A jump in bond yields might be the biggest threat to stocks.

The top 10 companies by market capitalization—consisting of primarily the AI-fueled tech stocks that make up the Magnificent Seven—account for a near-record 33.2% of the S&P 500 market value. The median P/E ratio of the top 10 stocks is 2.6 standard deviations above its long-term mean, while the bottom 493 stocks are 1.8 standard deviations above theirs.

The largest stocks are more overvalued, and the biggest risk is a rising 10-year Treasury yield. A steady decline in the 10-year Treasury yield since last October has made stocks attractive relative to bonds, but a resurgence in government bond yields could hurt the broader market, not just the mega-cap leaders. An increase in bond yields would put more pressure on equity valuations, not only for the top 10 stocks but also for many others that are trading at elevated P/E ratios.

The economy is being fueled by large amounts of government deficit spending and past stimulus. This may lead to stickier inflation and higher rates than markets expect.

JPMorgan Chase chief Jamie Dimon warned that U.S. interest rates could surge to more than 8% in the coming years as record U.S. debt and ongoing international conflicts complicate the fight to curb inflation. “Huge fiscal spending, the trillions needed each year for the green economy, the remilitarization of the world, and the restructuring of global trade—all are inflationary,” Dimon wrote in his annual letter to JPMorgan.

The ^GSPC is the S&P 500 index, a key proxy for the stock market.

Stocks have soared almost 30% since last October’s low, which was largely fueled by anticipation of an interest rate cut in March. However, three months later, these projections have been pushed out to perhaps July or September, or perhaps not at all this year. The stock market appears to ignore the recent change in when the Fed Funds rate will be cut, suggesting that corporate earnings will have to increase to close the gap. An unlikely scenario given estimates of slowing economic growth later this year.

A second source of economic growth estimates is from the Conference Board, published on April 11, 2024. They are expecting real economic growth to slow to under 1% in the second and third quarters of 2024—60% lower than 2023’s estimated growth. They believe growth will average 2.2% in 2024 and only 1.5% in 2025.

While we do not forecast a recession in 2024, we do expect consumer spending growth to cool and for overall GDP growth to slow to under 1% over Q2 and Q3 2024. Thereafter, inflation and interest rates should gradually normalize, and quarterly annualized GDP growth should converge toward its potential of nearly 2% in 2025.

US consumer spending held up remarkably well in 2023 despite elevated inflation and higher interest rates. However, this trend is already beginning to soften in early 2024. For instance, retail sales growth over the first few months of the year has been weak. Gains in real disposable personal income growth are softening, pandemic savings are dwindling, and household debt is increasing. Consumers are spending more of their income to service debt and delinquencies are rising. Additionally, the growth in ‘buy now, pay later’ plans may also weigh on future spending as bills come due. Thus, we forecast that overall consumer spending growth will slow in Q2 and Q3 2024 as households struggle to find a new equilibrium between income, debt, savings, and spending. While we anticipate labor market conditions to soften over this period, we do not expect them to deteriorate. As inflation and interest rates abate, consumption should expand once again in late 2024.

The Federal Reserve and economists have been consistently wrong about inflation and recessions.

The expected recession did not occur in 2023. The consensus among Wall Street analysts and Federal Reserve economists was incorrect, likely due to the wealth effect resulting in more consumer spending than anticipated. Additionally, substantial government stimulus remains in the system. The Federal Reserve kept interest rates too low for too long, contributing to high inflation and elevated interest rates today. The Fed’s quantitative tightening has been in place for the last two years and will continue until they make the first rate cut.

Savings increased to $2 trillion during the peak of the helicopter money from government but have now been largely spent. Credit card debt has soared to over $1.13 trillion, with defaults increasing as well. According to the Federal Reserve, the average credit card interest rate on accounts with balances that assessed interest was 22.75%.

We have been living on borrowed time, fueled by massive deficits and government spending, which accounts for about 50% of the growth when considering higher regulatory compliance costs.

As stimulus spending eventually tapers off, less consumer spending is expected in the coming years. It is also likely that corporate earnings expectations will diminish over the next few quarters.

There is an old saying on Wall Street: “The market moves up on an escalator but falls like an elevator.” In other words, it falls suddenly.

The Fed is likely to cut the federal funds rate later than originally expected, with fewer cuts anticipated. The initial consensus projected six cuts starting in May, which contributed to the market’s upward movement. However, due to hotter-than-expected inflation, expectations have shifted to only one or two cuts this year, with the first cut (25 basis points) expected in July or even September.

The longer interest rates remain high, the greater the negative impact on GDP growth, consumer spending, and corporate earnings. Another risk is the soaring crude oil and gasoline prices, which have increased by over 50% since President Biden took office. His anti-fossil fuel policies are a primary reason for the high energy prices.

Food prices are 36% above 2019 levels, causing financial struggles for many Americans, especially the bottom 50% of income earners.

Inflation has risen 19% since Biden took office, though this may understate real inflation when higher interest rates are considered. In contrast, inflation averaged 2% during Trump’s four years in office, and real wage gains were higher, particularly for the bottom 50% of income earners.

People who own assets such as housing and stocks are faring well, which is why they continue to spend. The wealth effect occurs when assets appreciate, as there is a high correlation between consumer confidence and real estate. People tend to spend more when their equity increases, approximately 3 cents more for every dollar increase in the stock market and housing prices.

The wealth effect may reverse as stock market and housing prices fall. A slow decline in real estate values is anticipated over the next few years. For example, housing values have fallen 11% in Austin since their peak (60% higher) and are about 30% too high in Tennessee and nationwide given lower inflation-adjusted income levels since Biden has been in office.

Cash may be king in the short term as the stock market appears to be on the cusp of a correction.

The good news for investors in money market accounts linked to short-term Treasuries is that they will have funds available to deploy when the market eventually corrects. A 5% risk-free rate seems like a more prudent choice at this point.

In my opinion, the opportunity costs for those fully invested in the stock market are too high. A sound strategy is to invest in the short end of the yield curve, such as 1–2-year Treasury bills, and wait until the market corrects to a more normalized level, which is a function of the 10-year Treasury yield and corporate earnings.

Interest rates have been rising largely due to the massive amount of debt the government must issue to fund $2 trillion in annual deficit spending expected for the next decade.

There will be upward pressure on interest rates as the net interest payments continue to increase as a percentage of GDP. Debt servicing costs are rising rapidly.

The 10-year Treasury yield could easily rise to 5% or higher, making it a good entry point to invest in this note. If the rate falls to 4%-3.5%, the note will appreciate by 10%-15%, in addition to the coupon rate. This is a tactical trade because rates are likely to fall during periods of slower economic growth.

Investing in the long end of the yield curve is not a good long-term investment, as rates will likely rise in subsequent years due to the government issuing large amounts of debt to finance unsustainable deficits.

The period from 2009 through 2021 was characterized by declining and ultra-low interest rates. This had profound ramifications, including influencing which investment strategies would thrive.

In 2022, the Fed began raising interest rates to curb inflation, marking a shift from the easy money conditions of the previous years. While temporary easing may occur in response to recessions, it is unlikely that we will return to the ultra-low interest rates of the past decade and a half.

This means that the investment environment in the coming years will likely involve higher interest rates than those observed in the last 15 years. As a result, asset values will need to be repriced, potentially triggering a reversal of the wealth effect that could last for many years.

Thanks for the feedback, George. Market shifts indeed! The only constant is change and understanding the shifting marketplace is an opportunity to profit...or lose money. My viewership is not as great on SubStack as it once was on the other social media platforms. I was deplatformed when censorship was at its peak and my readership was in the millions. However, it matters not because the research and commentary are for my own benefit and others who may be interested in the topics I cover. Thank you for all of your help.

An insightful and balanced overview of today's economy, emphasizing both the opportunities and risks in housing and stock markets. A must-read for anyone wanting to stay informed and prepared for potential market shifts!