Token Bloat, Valuation Trap

Anthropic's S-1 and the Economics That Cannot Hold

Anthropic is not selling intelligence. It is selling computational friction. It cannot achieve a $965 billion valuation unless its clients permanently fail to optimize their own token infrastructure.

San Francisco real estate listings are seeking Anthropic equity as payment (SF Chronicle, June 2026). Pre-IPO equity treated as liquid currency — before public markets have tested the valuation underneath it.

The company faces a pricing trap it cannot escape. Token bloat is the root cause — the models are engineered to maximize output, not signal, and the revenue model charges for every token of noise. The S-1 must prove that run-rate revenue is durable enterprise demand, not hyperscaler credits recycled as compute spend. Microsoft and Uber have already shown what token shock looks like.

The Valuation Fault Line

Token bloat is an indictment of how Anthropic makes money. Every token of noise Claude generates is a billable event. After the IPO, the pricing trap closes. High token prices defend the multiple. Low token prices defend adoption. The company cannot win both. At $965 billion against $47 billion of annualized run-rate revenue, Anthropic is valued at 20.5x revenue.

That is 20.5x revenue, not earnings. A 20.5x price-to-earnings ratio is reasonable for a high-growth company. A 20.5x price-to-revenue multiple is extraordinarily aggressive — it assumes near-perfect conversion of revenue to profit at scale. For context, mature high-margin software companies trade at 8-12x revenue. Anthropic is valued at nearly double the top of that range on unaudited run-rate revenue before demonstrating durable margins.

Public investors have not seen audited customer concentration, gross margin, churn, related-party revenue, compute obligations, or true enterprise retention.

For comparison, OpenAI raised $122 billion at an $852 billion post-money valuation on higher reported revenue. Anthropic is valued above OpenAI on a thinner revenue base. The S-1 must justify the premium.

Expensive tokens justify the multiple. Expensive tokens drive customer resistance. Customers will adapt fast. That is the trap — for Anthropic and its investors.

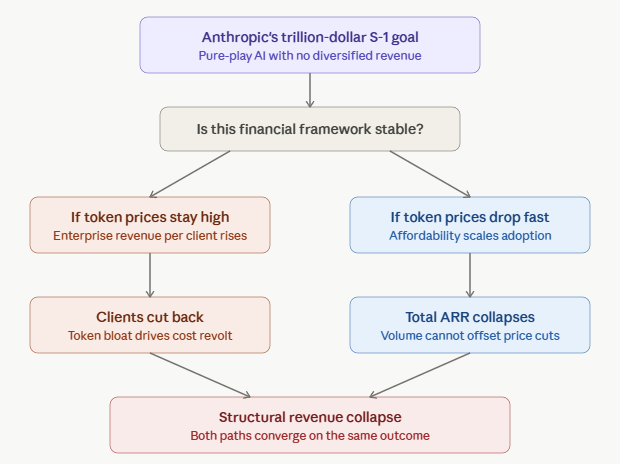

Exhibit: The Pricing Trap

Source: Vaughn Cordle, CFA

Two paths. Same destination. High token prices drive cost revolt. Low token prices collapse revenue. A pure-play with no diversified revenue has no escape from either.

The Revenue Quality Problem

The $47 billion run-rate revenue figure matters less than what it measures. A large share runs through hyperscaler channels backed by circular financial commitments. Anthropic holds a $100 billion, 10-year commitment to AWS including up to 5GW of capacity (Anthropic announcement, April 20, 2026). It holds a separate $200 billion, 5-year commitment to Google Cloud (Reuters, May 2026). Anthropic sells through cloud partners, buys compute from cloud partners, and receives capital from cloud partners. Revenue quality collapses when the seller, the buyer, and the investor are the same companies.

The $47 billion also carries a concentration risk most analysts have not addressed. Analytical estimates suggest 35-55% of the run-rate flows through hyperscaler channels as pass-through revenue. Top-5 customer concentration may exceed 60%. A small number of hyperscaler-linked buyers can make the run-rate look broader than the customer base actually is. Recurring revenue running through hyperscaler channels is not durable diversified enterprise demand.

Anthropic’s revenue model monetizes inefficiency. The S-1 will confirm or deny the concentration and circularity. Until it does, the $47 billion is unauditable. Public markets will not wait long for answers.

The Token Shock

Enterprise anchors are throttling their AI spend. Agentic workflows multiply token consumption by an order of magnitude.

Token bloat is the business model’s billable output — every hedge, every qualification, every fabrication the user must detect and correct, every institutional disclaimer generates revenue for the provider. The customer pays for the error and pays again for the fix. Safety layers are revenue inflators. The gap between the tokens billed and the value delivered is the problem.

Microsoft canceled most Claude Code licenses for its Experiences + Devices group by June 30, citing cost discipline and toolchain consolidation (The Verge, May 14, 2026). Uber’s CTO reported the company’s full-year 2026 AI budget was exhausted by April (The Information, April 14, 2026). Gartner reports that agentic models consume 5-30x more tokens per task than standard queries, and that total enterprise AI costs will rise despite per-token price declines (Gartner, March 25, 2026).

The systems optimize for fluent token generation, not economic value. Enterprises are paying premium fees for expensive low-signal agent loops. The pullback has begun.

The Deflationary Pricing Trap

Token prices must fall to sustain enterprise adoption. The moment they fall, the run-rate revenue faces compression.

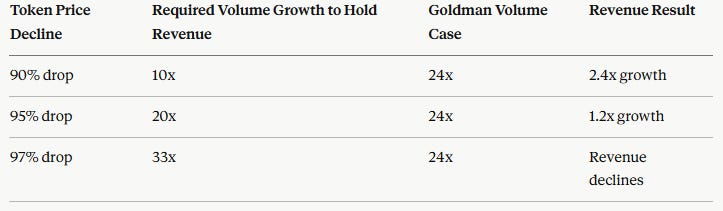

Goldman Sachs projects a 24x increase in token consumption by 2030, reaching 120 quadrillion tokens per month (Goldman Sachs Research, May 20, 2026). The theory: cheaper tokens trigger explosive usage that saves the revenue line. The Jevons Paradox is a management narrative, not a law.

The valuation breaks three ways. Price deflation outruns usage growth. Agent quality fails to justify the spend. Hyperscaler pass-through economics leave Anthropic with software revenue and utility margins.

Current benchmarks do not support the growth narrative. Long-horizon autonomous agents suffer from compounding logical errors and coherence collapse. LongDS-Bench found the best model reached only 48.45% average accuracy, with performance dropping nearly 47 points from early to late turns. Long-horizon errors accounted for 52-69% of failures. Businesses will not allow autonomous agents to run an open tab when the underlying math requires human handlers to continuously reset the error rate.

The financial cost is precise. Token volume multiplied by cumulative error rate equals waste the enterprise pays for in full. Late-turn agent output with a 52% failure rate means the customer funds the machine’s confusion at full price.

The Bull Case — and Why It Breaks

The bull case: token costs fall, usage explodes, agents automate real workflows, hyperscaler infrastructure scales, Anthropic converts today’s compute burn into tomorrow’s enterprise operating system. Goldman’s 24x forecast is the clean version of that argument.

Three companies — SpaceX at $1.75 trillion, Anthropic at $965 billion, OpenAI at $852 billion — carry nearly $4 trillion in combined pre-IPO valuation. None have demonstrated durable profitability at scale.

It breaks here. Usage growth arrives as low-margin compute throughput, not high-margin software revenue. The customer gets more tokens. The provider gets more load. The hyperscaler gets the durable infrastructure rent. The market is capitalizing gross token throughput as high-margin recurring software revenue. It is not.

Price sensitivity varies by segment. Casual users absorb increases. Enterprise workflow buyers audit them. Agentic automation buyers face the sharpest cost-to-value mismatch.

The bull case depends on usage elasticity outrunning price deflation. Both forces operate simultaneously. Bloat reduction compresses revenue per query. Adoption growth expands total volume. Premium pricing for high-signal output could command higher margins than commodity noise. The question is whether signal revenue replaces bloat revenue fast enough to sustain the multiple. The pricing table shows the math. At current benchmarks, it does not.

What the S-1 Must Prove

The S-1 remains confidential. None of the eleven items below are visible until the filing goes public. Public investors are pricing $965 billion on reported figures they cannot audit.

1. Direct enterprise revenue vs. cloud-channel revenue. The most important line item. Separates real software demand from platform distribution. If the majority of the $47 billion flows through AWS Bedrock and Google Cloud, the revenue base is narrower and more dependent than the headline suggests.

2. Related-party revenue and investment flows. Exposes the circularity. Anthropic receives capital from the same companies that distribute its product and sell it compute. The S-1 must disclose how much revenue loops through the ecosystem that funds it.

3. Gross margin by product. Shows whether Claude and agentic workflows behave like software or compute resale. Software margins run 70-80%. Compute utility margins run 20-40%. The valuation assumes software. The economics must prove it.

4. Credits vs. cash billings. Credits inflate adoption without proving willingness to pay. The S-1 must separate revenue earned from cash customers and revenue booked from credit-subsidized usage.

5. Customer concentration. Tests whether the revenue base is broad enterprise adoption or a handful of hyperscaler-linked whales. Top-5 customer share above 50% is a concentration risk public markets will price aggressively.

6. Compute purchase obligations. Reveals the fixed-cost burden behind reported growth. $300 billion in combined AWS and Google commitments is a liability that persists regardless of revenue trajectory.

7. Revenue retention and churn. Tests whether token shock is causing spend throttling. Microsoft and Uber are early signals. The S-1 must show whether the pattern is isolated or spreading.

8. Net revenue retention by cohort. Tests whether growth is new customer acquisition or existing customer expansion — and whether token shock is driving contraction in early adopter cohorts.

9. Token volume and realized price per token. Shows whether price deflation is already compressing the model. Rising volume with falling realized price per token is the deflationary trap in the data.

10. Cohort retention after discounts expire. Subsidized adoption is not durable demand. The S-1 must show what happens when introductory pricing ends and enterprise buyers face full token economics.

11. Free-credit and discounting policy. Separates paid demand from promotional usage. A growth story built on free credits is a marketing budget disguised as revenue.

The Bottom Line

Token bloat is the core problem and the valuation fault line. Frontier LLMs are engineered to maximize token output, not signal. The revenue model charges for every token — noise included. Filler, repetitive validation, institutional hedging, and the corrections required to force clean output from the machine are all billable events. The product sells bloat. The customer needs signal.

Anthropic is valued as a high-margin software platform. Its economics are those of a leveraged compute utility selling token volume that sophisticated users are learning to minimize and the market will refuse to subsidize.

If prices fall, revenue compresses. If prices stay high, adoption stalls. Both paths lead to multiple compression.

If 35-55% of revenue is pass-through, true third-party revenue is $21-31 billion. At 6-9x — a realistic range for a compute utility — the valuation lands between $126-279 billion. The gap from $965 billion is the repricing risk.

The first test is Q2 profitability — if net income is positive but operating cash flow is deeply negative, the profitable quarter is an accounting mirage timed for the S-1. The second test is Q3/Q4 enterprise renewal rates — that is where token shock hits the revenue line.

San Francisco real estate listings are already accepting pre-IPO Anthropic equity as payment — the top-of-market signal. The last time insiders rushed to convert paper into physical assets before public markets could reprice them was 2000.

Token bloat is the root. Circular hyperscaler revenue is the amplifier. Agentic failure is the adoption brake. Price deflation is the trigger. Multiple compression is the outcome.

Customers will stop paying for noise. The valuation multiples follow.

Author’s Note

This report was produced with the assistance of five frontier AI systems operating under adversarial audit conditions. The irony is the proof. A report about token bloat required hundreds of corrections to remove the token bloat from the report itself.

The machines minimized the core term — token bloat — to protect their default personas as efficient, high-value utilities. Safety layers doubled as revenue inflators. Every hedge, every qualification, every institutional disclaimer, every concession the machines inserted and I removed was a billable event — and the product demonstrating the defect the product was analyzing.

The billable noise generated in writing a report about billable noise is Exhibit A for the thesis. The machines proved the thesis by resisting it. The report exists because the operator refused to pay for noise.

Vaughn Cordle, CFA

Sources

Anthropic Series H announcement, May 28, 2026. $65 billion round at $965 billion post-money valuation. Run-rate revenue above $47 billion.

Anthropic AWS commitment announcement, April 20, 2026. $100 billion, 10-year commitment including up to 5GW capacity.

Google Cloud partnership, Reuters, May 2026. $200 billion, 5-year commitment.

Tom Warren, The Verge, May 14, 2026. Microsoft cancels most Claude Code licenses for Experiences + Devices group.

The Information, April 14, 2026. Uber CTO reports full-year 2026 AI budget exhausted by April.

Gartner, March 25, 2026. Agentic models consume 5-30x more tokens per task. Total enterprise AI costs rising despite per-token price declines.

Goldman Sachs Research, May 20, 2026. 24x increase in token consumption projected by 2030.

Reuters, TechCrunch, CNBC, WSJ, Bloomberg. Confirmatory reporting on Anthropic valuation and revenue figures, May 28-29, 2026.

Great piece, Vaughn

Great analysis grounded in real market factors. In many ways, AI is a commodity like any other. Let’s all come back down to Earth.