Why airline consolidation lowered fares

Why airline consolidation lowered fares

To earn its cost of capital over the 2000-2009 business cycle, the industry would have had to raise fares for the average seat by 11%. Consolidation was the only way to lower costs and fares.

“Wall Street has consolidated into 5 giant banks. Airlines have merged from 12 carriers in 1980 to 4 today. A handful of drug companies control the pharmaceutical industry. Four giants control over 80% of meat processing. The evidence of corporate concentration is everywhere.” – Robert Reich@RBReich

Robert Reich is typically on the wrong side of the argument on the subject of economics, markets, and corporate America, but he is right about the higher concentration in many industries. However, the assumption that it always leads to higher prices is not supported by the facts.

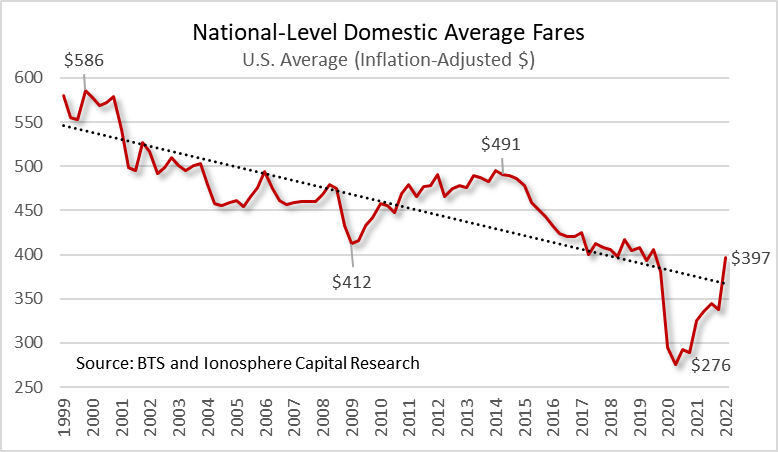

The airline industry consolidated between 2005 and 2013 after years of losses between 2000 and 2009. The big six airlines became the big three and there were many bankruptcies and mergers in the smaller regional airline sector.

Industry concentration, as measured by the Herfindahl-Hirschman Index (HHI), increased by 46% during this time but average airfares fell 17% by 2019, adjusted for inflation and after consolidation.

HHI quantifies market concentration to determine if a market provides healthy competition or is close to being a monopoly. An industry with an HHI of less than 1,500 is considered competitive. The airline industry's Available Seat Mile (ASM) HHI increased from a business cycle low of 900 after 9/11 (2002-2006) to 1,318 by 2013.

After the Nasdaq bubble burst in March 2000 and terrorists attacked the U.S. on 9/11, 2001, the airline industry suffered excessive capacity and massive losses. In the years after 9/11, when revenues collapsed, the airlines were trapped in a labor cost bubble. Only the threat of bankruptcy could lower labor costs in the industry.

At the time I argued that the industry needed to consolidate to survive and return to viability. (See my 2010 writeup of a meeting with Former American Airline CEO Bob Crandall and Congressman James Oberstar, Opposition to Airline Mergers Is Based on Three Premises.)

To earn its cost of capital over the 2000-2009 business cycle, the industry would have had to raise fares for the average seat by 11%. This was not possible given an economic contraction that bottomed during the Great Recession of 2008.

Bankruptcies, mergers, and consolidation – increased concentration – were the only way to lower costs and fares. The consensus argument that higher concentration would result in higher fares was false and based on a dubious understanding of the industry.

Consolidation increased the scope and scale of economies, which benefited airline shareholders, employees, and consumers. Before consolidation, the industry competed away profits, the result of excessive seat capacity. But higher industry concentration produced profits to buy new fuel-efficient aircraft, which lowered fuel and maintenance costs and improved reliability.

These are the reasons airfares fell after consolidation. Labor eventually received big pay raises and the airline industry recovered.

Opposition to Airline Mergers Is Based on Three Premises

By Vaughn Cordle, CFA - May 27, 2010

A Reply to Bob Crandall and Congressman Oberstar

Several themes keep surfacing from different participants in this discussion.

The first theme (see Bob Crandall) is that excess capacity doesn’t exist. We want to be clear that we are not using this term subjectively, but rather that we are working from a quantifiable definition. In the airline industry excess capacity is capacity over-and-above the level compatible with the industry earning its cost of capital over a full business cycle.

To earn its cost of capital over the most recent business cycle (2000-2009), the industry would have had to raise fares for the average seat by 11%. Calculating consumer demand response over this decade (as prices rise, consumer demand falls, known as price elasticity), we see that this price level is consistent with a 7% lower capacity (holding load factors constant). Hence, the definition of excess capacity.

The second theme (see both Congressman Oberstar’s and Bob Crandall’s comments) is that more mergers cannot be relied on to remedy the industry’s ills. For reasons we laid out in our white paper, we believe that absent mergers, the only alternative is the slow liquidation we are already witnessing.

Allowing one or more large network airlines to fail – the implicit alternative if mergers are taken off the table – is not a practical solution for the airlines’ stakeholders and it doesn't solve the industry’s problem of inadequate profitability and severely damaged balance sheets.

This opposition to mergers is based on three premises

The first is that mergers don’t always work. We agree but would argue that it is not the government’s job to second-guess commercial thinking. We would, however, note that the likelihood of success is reduced if the merger is delayed or if approval requires the shedding of too many assets.

The second is that mergers don’t create value by themselves but only cannibalize market share. Mergers that better align carriers with both national and global markets do create value, particularly in an era of global alliances.

The third is that mergers result in “fewer customer alternatives” and are harmful to consumers. This is proved wrong by the large numbers of domestic and international competitors that will remain. Bob makes the point that low-cost carriers (LCCs) will continue to compete “aggressively” against the networks. This is true, but we would add that given the LCC market penetration we anticipate over the next several years, network pricing power will be reduced even further. This supports the need for additional [network] mergers, to increase industry pricing power. The system can only profitably support three large networks, not four or five.

Bob Crandall did talk about the need to “Negotiate a level playing field internationally.” This was the AA (UAUA) mantra in Crandall’s day. But that argument is obsolete. Now there are Open Skies with Europe, Japan, India, and much of the rest of the world. This administration, like the three before, has embraced this policy. Is he suggesting the policy be rescinded, ATI removed and alliances disbanded? We will argue that the US network carriers have neither the capital nor clout to unilaterally provide for this nation’s need for global access.

Congressman Oberstar is concerned about small communities that will lose air service. We argue that this will be the case if industry consolidation is precluded. It takes viable and healthy large network airlines to serve small markets. LCCs have shown little interest in providing such services.

Finally, Congressman Oberstar believes that the Delta (DAL) /Northwest merger created an impetus for additional mergers in the industry. We believe that additional mergers are the result of the same pressures that led to the Delta/Northwest merger.

While the consumer has benefited from the fall in airfares, the industry has suffered. In today’s dollars, the industry lost $70 billion over the last decade. Other stakeholders, however, must also be considered, including those small communities and the capital providers. We have grown so used to this industry losing billions of dollars year after year that we are now inured to the threat those losses pose to the service we want. If something cannot continue forever, it won’t.

There are areas we agree on. For example, we agree that updating our infrastructure is a valid goal, but we note that it is far in the future before this can be achieved.

Mergers are not the ideal solution but are better than the alternative, which is a continuation of the downward spiral in product quality and viability and the loss of even more small market services.