The AI Valuation Trap

Token Bloat, Circular Capital, and the Economics That Cannot Hold

Part One of The Valuation Trap Series

The AI ecosystem cannot be valued company by company. It must be valued as a system of capital flows.

Pure-play AI labs create the hype. Integrated companies fund the infrastructure. Wall Street packages the story. Investors buy the multiple.

That is the machine.

The market is treating AI as high-margin software. The economics look more like a capital-intensive utility built on chips, data centers, power grids, cloud credits, depreciation schedules, and subsidized token consumption.

The largest players are guiding toward more than $700 billion of AI-related capital expenditure for 2026 alone. These companies now drive the Wilshire 5000, S&P 500, Nasdaq, and the ETFs tied to them. They are no longer just technology companies. They are the backbone of an overcapitalized infrastructure boom.

This report separates durable value from subsidized growth, circular revenue, token bloat, political bottlenecks, accounting stretch, ETF concentration, and IPO hype.

The Token Factory

Frontier AI models are token factories.

A token is a fragment of language. The model predicts one token after another. The more tokens it produces, the more it bills the customer.

Revenue rises with token volume. Customers need signal. The provider gets paid for output. The customer pays to eliminate noise.

This creates token bloat: excessive, repetitive, low-signal output that inflates billable usage without delivering proportional economic value. Whether by design or incentive, the result is the same. The provider books activity. The customer fights waste.

Token bloat is not a minor product flaw. It is the economic fault line.

Current revenue growth across the AI ecosystem depends heavily on token consumption that sophisticated users are learning to reduce. Better prompts, shorter workflows, smaller models, local inference, and tighter enterprise controls all attack the same line item: wasted token volume.

The industry needs token usage to explode. Customers need token usage per task to fall. Both cannot be true forever.

The AI Capital Loop

The AI ecosystem has two groups of players.

Pure-play AI companies — OpenAI, Anthropic, xAI, Mistral, and others — sell models and AI services. They have no large, profitable legacy business to absorb losses. Their survival depends on investor capital, cloud partnerships, and continuous belief in future scale.

Integrated companies — Microsoft, Google/Alphabet, Amazon, Oracle, Meta, SpaceX, and NVIDIA — have cash-generating core businesses. Cloud, search, advertising, e-commerce, satellite broadband, semiconductors, and enterprise software fund their AI ambitions.

The two groups are tied together. Pure-plays sell AI services through the integrated companies. The integrated companies supply the compute the pure-plays need. Hyperscalers invest capital. AI labs buy compute. Revenue moves through the system and loops back into infrastructure spend.

The circularity is the story. Hyperscalers invest in pure-plays. Pure-plays buy compute from hyperscalers. Hyperscalers book revenue. Pure-plays book revenue. Both report growth. The money moves in a loop. Fresh investor capital keeps the loop funded. The reported numbers look like independent demand. They are not.

Investors must ask one question: how much of the reported growth is independent customer demand, and how much is ecosystem recycling?

That question matters before every IPO.

Pure-Plays vs. Integrated Players

Pure-plays sell AI. They must make money from AI.

Integrated players can lose money on AI because other businesses fund the burn.

A pure-play AI company has no escape from unit economics. If token prices stay high, customers revolt. If token prices fall, revenue compresses. If agentic usage expands faster than value creation, enterprise buyers impose limits. If infrastructure costs stay high, margins look more like utility margins than software margins.

Integrated companies have more room. They can subsidize AI to defend cloud share, search, advertising, e-commerce, or enterprise software. They can absorb losses longer. They can use AI as a weapon against competitors, even if the direct AI business fails to earn software margins.

Pure-plays and integrated players should not trade at the same multiple. One group can afford to burn capital. The other group must prove the fire becomes profit.

The Hype Engine — A Financial Psyop Against Retail Investors

This is a financial psyop against retail investors. Name it precisely and the mechanism becomes visible.

The operation has three components: narrative construction, institutional amplification, and retail distribution.

Pure-play labs create the growth narrative. Wall Street banks convert the narrative into IPO math. Private investors mark up the rounds. Public investors receive the distribution.

Wall Street banks — at least 20 major firms participating in the current IPO wave — publish aggressive revenue projections that assume token bloat and subsidized usage continue indefinitely. These forecasts support extreme valuations. The AI companies get higher valuations and easier capital raises. The banks get underwriting fees, trading spreads, and future banking relationships. Retail investors get shares priced for perfection in businesses whose unit economics have never been publicly audited.

The operation positions investors’ beliefs above rigorous judgment — making sky-high multiples feel like consensus wisdom rather than speculative pricing. It works because every participant in the distribution chain has a financial incentive to keep the narrative alive and no participant has a financial incentive to puncture it before the IPO closes.

The banks do not need the forecast to be right forever. They need it to be persuasive during distribution.

Every player in the distribution chain gets paid before the public investor learns whether the economics work.

The Token Shock

Enterprise anchors are throttling their AI spend.

Microsoft canceled most Claude Code licenses for its Experiences and Devices group by June 30, citing cost discipline and toolchain consolidation (The Verge, May 14, 2026). Uber’s CTO reported the company’s full-year 2026 AI budget was exhausted by April (The Information, April 14, 2026). Gartner reports that agentic models consume 5 to 30 times more tokens per task than standard queries, and that total enterprise AI costs will rise despite per-token price declines (Gartner, March 25, 2026).

Agentic workflows multiply token consumption by an order of magnitude. Token bloat is the business model’s billable output — every hedge, every qualification, every fabrication the user must detect and correct, every institutional disclaimer generates revenue for the provider. Safety layers are revenue inflators. The gap between the tokens billed and the value delivered is the problem. The customer pays for the error and pays again for the fix.

The systems optimize for fluent token generation, not economic value. Enterprises are paying premium fees for expensive low-signal agent loops. The pullback has begun.

The Deflationary Pricing Trap

Token prices must fall to sustain enterprise adoption. The moment they fall, the run-rate revenue faces compression.

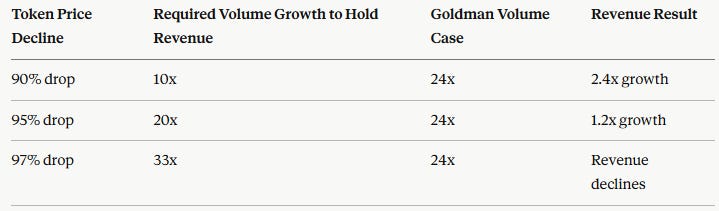

Goldman Sachs projects a 24x increase in token consumption by 2030, reaching 120 quadrillion tokens per month (Goldman Sachs Research, May 20, 2026). The theory: cheaper tokens trigger explosive usage that saves the revenue line. The Jevons Paradox is a management narrative, not a law.

The Goldman 24x consumption forecast only saves the revenue line if token prices fall no more than 90 percent. If competitive pressure, efficiency gains, and smaller models drive prices down 95 to 97 percent — a realistic outcome in a maturing commodity market — Goldman’s own volume projection produces revenue compression, not revenue growth. The bull case is built on a pricing floor assumption that the competitive dynamics of the market will not support.

Current benchmarks do not support the agent productivity assumption either. Long-horizon autonomous agents suffer from compounding logical errors and coherence collapse. LongDS-Bench found the best model reached only 48.45% average accuracy, with performance dropping nearly 47 points from early to late turns. Long-horizon errors accounted for 52-69% of failures. Businesses will not allow autonomous agents to run an open tab when the underlying math requires human handlers to continuously reset the error rate.

The financial cost is precise. Token volume multiplied by cumulative error rate equals waste the enterprise pays for in full. Late-turn agent output with a 52% failure rate means the customer funds the machine’s confusion at full price.

The valuation breaks three ways. Price deflation outruns usage growth. Agent quality fails to justify the spend. Hyperscaler pass-through economics leave pure-plays with software revenue and utility margins.

The Data-Center Political Wall

The AI buildout assumes capital can buy capacity on command.

It cannot.

DataCenterWatch reports that roughly $64 billion of U.S. data-center projects have already been blocked or delayed by local opposition. Gallup reported in May 2026 that seven in ten Americans oppose AI data centers in their local area. MultiState tracked 14 statewide data-center moratorium bills across 11 states, plus broader data-center legislation in 27 states. The Artificial Intelligence Data Center Moratorium Act introduced by federal lawmakers would halt all new facilities over 20 megawatts.

This is no longer a zoning nuisance. It is a political wall.

The industry is selling an 18-36 month capex story. Power systems do not move on that schedule. Grid interconnection, transmission upgrades, local permitting, water rights, tax incentives, ratepayer fights, and environmental review can stretch five to ten years.

AI companies can announce data centers faster than communities can approve them. Hyperscalers can raise capital faster than utilities can add firm power. Wall Street can model capacity faster than the grid can deliver electrons.

Every delayed project pushes revenue further into the future while depreciation, financing costs, and investor expectations keep moving now.

The political wall turns AI capex from an execution plan into a permitting bet.

This is the constraint that almost no sell-side model prices. The Goldman 24x token consumption forecast assumes the infrastructure exists to deliver it. The infrastructure does not exist. Building it requires overcoming regulatory barriers that the AI industry has no mechanism to fast-track.

The Depreciation Mismatch

AI infrastructure is being depreciated like long-lived infrastructure while the hardware cycle behaves like short-lived technology.

Microsoft moved server and network equipment useful lives from four years to six years. Meta extended most servers and network assets to 5.5 years and said the change would reduce 2025 depreciation expense by roughly $2.9 billion. Amazon moved some server and networking assets from six years back to five years after citing faster technology development in artificial intelligence and machine learning.

Three companies. Three decisions. Two stretched the schedule to flatten expenses. One shortened it after the evidence forced a correction.

If GPUs remain economically useful for five or six years, the accounting holds. If competitive obsolescence hits in two or three years, current earnings overstate economic reality. When GPU generations compress faster than depreciation schedules, the write-down cycle accelerates. Microsoft, Google, and Amazon are each carrying hundreds of billions in AI infrastructure at book values that assume 2028 and 2029 productivity. If the hardware is economically obsolete by 2026, the write-downs arrive before the revenue justifies the investment.

Longer useful lives lift reported margins today. Shorter economic lives force write-downs, lower operating income, and weaker free cash flow tomorrow.

Public investors are being asked to buy software multiples on a hardware cycle that may require constant reinvestment.

The S-1s will not show this. The 10-Ks will, eventually.

Depreciation is the hidden variable in AI earnings quality.

The Retail ETF Concentration Trap

The AI trade is not confined to individual stock pickers. It is embedded in ETFs.

Gallup’s 2025 investor survey found that retail ownership of technology stocks is at its highest concentration since 1999. AI-themed and tech-heavy funds have absorbed more than $180 billion in retail capital in the past 18 months. NVIDIA, Microsoft, Apple, Amazon, Meta, Alphabet, Broadcom, Tesla, AMD, and Micron dominate the allocations. Retail flows have chased the same trade through thematic ETFs, semiconductor ETFs, Nasdaq products, and leveraged vehicles.

The structure creates forced correlation. When AI leaders rise, the ETFs pull in more money and buy more of the same stocks. When the leaders reprice, the same structures sell the same names together.

Retail investors think they own the future. They own the same factor, repackaged ten different ways.

The problem is not that retail investors are buying AI. The problem is that they are buying it through vehicles that do not distinguish between integrated players with durable cash flows and pure-plays with circular revenue and no proven unit economics. When the repricing arrives, it will not discriminate between the two. The ETF structure guarantees correlated selling pressure across the entire category.

The next repricing will not stay inside one IPO or one stock. It will move through ETFs, options, leveraged products, model portfolios, retirement accounts, and passive index flows. The selling will look diversified on the statement and concentrated on the tape.

Retail investors in AI-weighted ETFs are not buying the productivity revolution. They are buying the hype cycle’s distribution mechanism. The S-1 filings will not tell them this. This is how retail inherits the valuation risk after private markets and insiders have already marked up the assets.

The Bull Case — and Why It Breaks

The bull case: token costs fall, usage explodes, agents automate real workflows, hyperscaler infrastructure scales, and pure-plays convert today’s compute burn into tomorrow’s enterprise operating system.

It breaks here. Usage growth arrives as low-margin compute throughput, not high-margin software revenue. The customer gets more tokens. The provider gets more load. The hyperscaler gets the durable infrastructure rent. The market is capitalizing gross token throughput as high-margin recurring software revenue. It is not.

Three companies — SpaceX at $1.75 trillion, Anthropic at $965 billion, OpenAI at $852 billion — carry nearly $4 trillion in combined pre-IPO valuation. None have demonstrated durable profitability at scale.

The Bottom Line

The AI boom is real. The valuation structure is not.

Token bloat is the core problem. Frontier LLMs are engineered to maximize token output, not signal. The revenue model charges for every token — noise included. The product sells bloat. The customer needs signal.

The pure-plays are valued as high-margin software platforms. Their economics are those of leveraged compute utilities selling token volume that sophisticated users are learning to minimize and the market will refuse to subsidize.

If prices fall, revenue compresses. If prices stay high, adoption stalls.

Token bloat inflates usage. Usage inflates revenue. Revenue inflates valuations. Valuations justify capital raises. Capital raises subsidize more token bloat.

The loop works until customers stop paying for noise, communities stop approving data centers, GPUs stop supporting the accounting schedule, and public investors stop buying private-market marks.

Public investors are being asked to capitalize token waste, subsidized usage, circular funding, political bottlenecks, depreciation stretch, ETF concentration, infrastructure scarcity, and IPO hype as if they were durable software profits.

AI may transform the economy. That does not make every AI valuation investable. The market is pricing the future as if the hardest problems have already been solved.

They have not.

This is the ecosystem. Part Two applies it to the most dangerous IPO in the pipeline.

Sources

Anthropic Series H announcement, May 28, 2026. $65 billion round at $965 billion post-money valuation. Run-rate revenue above $47 billion.

Anthropic AWS commitment announcement, April 20, 2026. $100 billion, 10-year commitment including up to 5GW capacity.

Google Cloud partnership, Reuters, May 2026. $200 billion, 5-year commitment.

Tom Warren, The Verge, May 14, 2026. Microsoft cancels most Claude Code licenses for Experiences + Devices group.

The Information, April 14, 2026. Uber CTO reports full-year 2026 AI budget exhausted by April.

Gartner, March 25, 2026. Agentic models consume 5-30x more tokens per task.

Goldman Sachs Research, May 20, 2026. 24x increase in token consumption projected by 2030.

DataCenterWatch. $64 billion in U.S. data-center projects blocked or delayed.

MultiState. 14 statewide data-center moratorium bills across 11 states. Broader data-center legislation in 27 states.

Gallup, May 13, 2026. Seven in ten Americans oppose AI data centers in their local area.

Gallup, 2025. Retail ownership of technology stocks at highest concentration since 1999.

Microsoft 10-K. Server useful life extended from four to six years.

Meta 10-K. Server useful life extended to 5.5 years. 2025 depreciation reduced by approximately $2.9 billion.

Amazon 10-K. Server useful life reduced from six to five years citing faster AI development.

LongDS-Bench benchmark data. Best model 48.45% accuracy. Performance dropped 47 points early to late turns.

Great read. Every new technology must eventually pass the cost/benefit analysis for the first wave to survive. If AI follows the path of the railroad industry, there will be a lot of blood on the table before the benefit supports the reduced cost. And that assumes the benefit will pay for variable costs.

I’m concentrating on the picks and shovels supporting the tech, and that may not be an entirely safe play.

Brilliant analysis.

In capital intensive/highly regulated/politicized businesses, the winners are the ones who can actually raise the capital, get the regulatory approvals, and deal with the grass roots politics.

Failure to clear these hurdles in a timely manner dooms the initiative even when the underlying idea is superior.

In business you don’t get what you deserve; you get what you negotiate.