The Unaffordable Care Act: ObamaCare is an abysmal failure

ObamaCare failed to solve the critical health care problems it was supposed to address. Even worse, it has compounded many of the problems it was meant to fix.

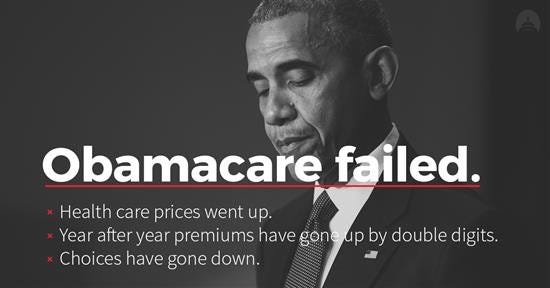

Former President Barack Obama visits the White House today, his return pegged to an event marking the 12th anniversary of the Affordable Care Act, a signature legislative achievement under his administration. Obamacare more than doubled health insurance costs for workers and families, with the national average premium increasing by 136 percent from 2013 to 2021. The average out-of-pocket deductible for single coverage increased 62 percent. The average annual cost of health insurance in the USA is $7,470 for an individual and $22,221 for a family in 2021, according to the Kaiser Family Foundation. Obamacare has fallen woefully short in Obama’s misguided ambition to reduce health insurance premiums by $2,500 per year.

Twelve years after the passage of Obamacare, Americans buying health insurance under the law are worse off financially than before the health law was enacted. Data on how much Americans paid for their health insurance confirm that the ACA’s mandates and regulations dramatically increased the cost of individual market health insurance in almost all states. At the event, President Biden unveiled expansions to that law. Obama’s visit comes as Biden faces the lowest approval rating of his presidency and months of low popularity and disapproval linked to his handling of the ongoing war in Ukraine.

MIT economist Jonathan Gruber, one of the architects of the Affordable Care Act, or Obamacare, was caught insulting voters and suggesting their ignorance was exploited by those pushing passage of the health care law. “It’s a very clever, basic exploitation of the lack of economic understanding of the American voter. Call it the stupidity of the American voter.”

Now is a good time to review Obama’s healthcare law and its many failures—on the very day President Biden unveils expansions to the law. The analysis, originally published on October 12, 2020, is still relevant given Biden’s expansion of the ‘unaffordable’ healthcare law.

If Obamacare was Obama’s greatest ‘success’, imagine how bad the failures will be if the Democrats win in November and build upon one of the biggest policy failures in America’s history. Even its supporters acknowledge its failures, which is why many of them have given up on Obamacare and are calling for more government through Medicare for all. This, of course, would be another policy disaster.

Note: Obamacare supporters tend to conflate subsidized and unsubsidized health care, denying or dismissing the idea that Obamacare has, in large measure, driven up the cost of insurance for Americans. Only 9.3m (87% of 10.7m) people, who purchased insurance on the Marketplace, are subsidized. Unfortunately, the majority of Americans are paying budget-busting high premiums and out-of-pocket deductibles. As of 2020, over 297 million people in the United States had some kind of health insurance.

The Unaffordable Care Act: ObamaCare is an abysmal failure

Vaughn Cordle, CFA / October 12, 2020

The U.S. Census Bureau on health insurance coverage shows the number of uninsured Americans has risen significantly. As usual, critics of President Trump blame the Administration’s healthcare policies for this increase. But a review of key facts suggests the rising uninsured rate stems largely from Obamacare’s failure to deliver affordable health insurance premiums and has created a large number of uninsured.

While Obamacare—more formerly known as the Patient Protection and Affordable Care Act (ACA)—promised affordable health insurance for every American and even penalized those who refused to buy it, the law did nothing to control underlying costs. The very structure of the law which imposed billions of dollars in new, costly regulations also led to higher and higher insurance premiums.

As a result, when President Trump took office in 2017, average individual market health insurance premiums in states using HealthCare.gov had already doubled when compared to 2013, the year before Obamacare’s main regulations took effect. Average premiums went up by another 26 percent in 2018.

At the same time, individual market premiums were spiking—Centers for Medicare & Medicaid Services (CMS) data show a substantial enrollment drop among unsubsidized people on the individual market who do not receive federal premium tax credits. In just two years, from 2016 to 2018, unsubsidized enrollment declined by 2.5 million people, a 40 percent drop.

In its first decade ending March 2020, Obamacare failed to solve the critical health care problems it was supposed to address. Even worse, it has compounded many of the problems it was meant to fix—the law of unintended consequences in action. Then-candidate Barack Obama promised it would “cut the cost of a typical family’s premium by $2,500 a year.”

The actual results have proven that the opposite has occurred. According to the Department of Health and Human Services (HHS), “premiums have doubled for individual health insurance plans since 2013, the year before many of Obamacare’s regulations and mandates took effect.” Average individual market premiums more than doubled from $2,784 per year in 2013 to $5,712 in 2017—an increase of $2,928 or 105%. Obamacare has fallen woefully short in Obama’s misguided ambition to reduce health insurance premiums by $2,500 per year.

Obamacare supporters claimed it would drastically reduce the uninsured population. Unfortunately, this also has not happened. As of March of this year, there were roughly 28 million Americans without health insurance. And since the individual mandate, which forced Americans to purchase health insurance, has been repealed, the numbers have increased even more.

According to the Centers for Medicare and Medicaid Services (CMS), “Simply put, there are too many people without subsidies who cannot afford coverage under Obamacare.”

Why do so many Americans remain uninsured? CMS provides a typical example: “A 60-year-old couple making $70,000 a year—which is too high to qualify for Obamacare’s premium subsidy—is faced with paying $38,000, over half of their yearly income, to buy a silver plan with an $11,100 annual maximum out-of-pocket limit.” This is why over 20 million Americans are uninsured today. Facing a similar harsh reality, it was inevitable that, for millions of Americans, Obamacare’s affordability crisis would eventually show up in the rates of the uninsured.

In 2013, Obama promised, “If you like your health care plan, you’ll be able to keep your health care plan, period,” a pledge named Lie of the Year by PolitiFact. President Obama also repeatedly guaranteed voters, “If you like your doctor, you will be able to keep your doctor, period.” As it turns out, this promise was false and misleading. Even worse, “15% of plans offered on the exchanges exclude doctors from at least one kind of specialty” notes the National Institute of Health. Put another way, after Obamacare took effect, millions of Americans lost access to their doctors.

Obamacare, a one-size-fits-all centrally planned boondoggle, has failed because it lacks free-market principles. In the next decade, and for decades to come, the American health care system would function much more optimally if patients, not bureaucrats, were allowed to take control of their health care decisions.

Republicans are trying to turn the program and the money over to the states. This would make sense because states would be free to experiment and find ways to reduce costs and provide better services.

Democrats are pushing a political spin, which is that Obamacare is the best policy. They claim that the only reason premium and deductible costs keep exploding is because President Donald Trump repealed the individual mandate tax—which was nothing more than an unfair penalty on low-income families that can’t afford the high cost of the health laws mandates. But if Trump is to blame, why were the costs skyrocketing two years before Trump entered the Oval Office?

The predicted death spiral in the insurance market—higher costs cause more healthy people to drop coverage, which raises prices even more, and the cycle continues—is now irrefutably upon us. This law should be renamed the Unaffordable Care Act.

Critical facts about Obamacare:

Health insurance is more expensive than ever. In May 2017 the Department of Health and Human Services reported that average health insurance premiums doubled since 2013. How many family incomes doubled over that period?

In 2018 costs have risen by another 19 percent for high-cost plans and 32 percent for the cheapest plans, according to a study by the Urban Institute. Overall inflation for all other goods and services is running at 2 percent.

Entitlement spending has exploded. Obamacare has driven entitlement spending up much faster than expected. The projected budgetary cost of Obamacare subsidies and Medicaid expansions from 2018 to 2027 now totals $4.8 trillion. The Congressional Budget Office estimates that Obamacare and its Medicaid expansion are responsible for 44 percent of the projected future increases in entitlement spending.

Obamacare has not stopped rising health care costs. Instead of “bending the cost curve down,” national expenditures on health care continue to rise. The year before Obamacare was fully implemented, health care amounted to 17.2 percent of U.S. gross domestic product. Last year that tab grew to 18.3 percent—an increase of almost $200 billion in health spending. The latest forecast for 2025 is that medical expenses will reach almost 20 percent of GDP.

Americans are paying more for less health coverage. According to Kaiser, the average deductible for people with employer-provided health coverage was $1,221 compared to $303 in 2006. Usually, you pay higher deductibles for lower premiums. Under Obamacare, you pay more when you get your hospital bill.

Fewer insurance choices. According to federal and state data on insurer exchange options per county, more than 50 percent of our nation’s counties have only one insurer in 2018. Over 30 percent of counties are limited to two insurers. This means roughly 4 of 5 counties will have either just one or two Obamacare exchange insurers from which to choose.

Medicaid enrollment is exploding. The vast majority of Americans who have received insurance under the Obamacare law have enrolled in Medicaid. Medicaid enrollment has soared from 55 million to 74 million since 2013. Yet many physicians, health clinics, and hospitals don’t accept Medicaid. This means tens of millions of Americans often can’t choose the doctor, hospital, or treatment of their choice. Medicaid users in major cities experience an average denial rate of 47 percent. Mid-sized city Medicaid users have an average denial rate of 40 percent.

Nearly 30 million Americans are still uninsured. On April 1, 2014, standing in the Rose Garden at the White House, President Barack Obama claimed that the Affordable Care Act meant “everybody” would have health insurance. Today, some 30 million Americans remain uninsured. Why? Families can’t afford the insurance.

In 2012, the Congressional Budget Office estimated that Obamacare exchange enrollment would increase by 9 million by 2016. Instead, an underwhelming 400,000 increase occurred, which is a staggering 96 percent reduction in the anticipated growth of net-ACA exchange enrollment.

Obamacare continues to ignore obvious cost-saving alternatives. Obamacare does not allow patients to buy insurance across state lines, which would dramatically increase competition and lower costs. It does not allow small business-associated health plans. It limits low-cost health savings accounts options. It has no provisions for capping medical malpractice costs—because Democrats were bought off by the trial lawyers.

Preexisting Conditions?

Why have premiums skyrocketed so that only people receiving federal subsidies can afford to pay their insurance rates? A Heritage Foundation analysis provides a clear answer:

A cluster of [Obamacare] insurance-access requirements — specifically the guaranteed-issue requirement and the prohibitions on medical underwriting and applying coverage exclusions for pre-existing medical conditions — accounts for the largest share of premium increases.

In other words, the preexisting condition provisions have proven the largest factor in pricing millions of people out of their health insurance coverage. This means, ironically enough, such people now have no coverage should they develop any such condition.

The American people need to understand the effects of Obamacare. Liberals ignore or conceal the fact that families care more about the affordability of health coverage than about losing their coverage due to a preexisting condition. Reforms codified by the Trump administration will help provide portable and more affordable coverage to many Americans and represent one of several better solutions to tackle the preexisting condition problem.

The left’s “solutions” to Obamacare’s skyrocketing premiums represent more of the same — more taxes, more spending, and more subsidies to make coverage “affordable” for a select few. But sooner or later, the left will eventually run out of other people’s money. The Unaffordable Care Act’s failure to deliver demonstrates that the American people need and deserve a better approach than the left can devise.

Conclusions

Hundreds of billions of dollars have been spent; we have massively increased the size of the federal budget; we have subsidized insurance plans to get Americans to sign up for Obamacare; we have penalized people if they don’t buy Obamacare (until that law was repealed), but we still have almost 1 in 11 Americans without insurance.

If Obamacare was Obama’s greatest success, imagine how bad the failures will be if the Democrats win in November and build upon one of the biggest policy failures in America’s history. Thank Obamacare for the rise of the uninsured and the spike in healthcare costs.

Together the data show how Obamacare created an entirely new class of the uninsured—those with middle to higher incomes who don’t qualify for government subsidies and can’t afford coverage because of skyrocketing premiums.

Much of the news coverage has claimed that the increase in the number of uninsured was driven by the decline in people covered by Medicaid. Yet, this simply does not match the fact that the Census data also reported no statistically significant change in the number of uninsured with incomes lower than 138 percent of FPL, the people most likely to be eligible and enrolled in Medicaid. These numbers help explain why the uninsured rate went up at the same time the poverty level went down.

Unfortunately, even with a strong economy and labor market, Obamacare’s flaws cannot be fixed. The Trump Administration has enacted several reforms to promote more stable markets and more affordable coverage.

The rate of uninsured may continue to rise as long as Obamacare is in effect. Even its supporters have acknowledged its failures, which is why many of them have given up on Obamacare and are calling for more government through Medicare for all. This, of course, would be another policy disaster.

I was intrigued by the data and thought I'd do a comparison of what I've experienced with my current employer. I found a pay statement from late 2012.

2012 Employer cost for Medical/Health Insurance: $881.67/month low deductible plan

2012 Employee cost: $118.25/month

2022 Employer cost for Medical/Health Insurance: $1,374.88/month high deductible plan

2022 Employee cost: $116.09/month

One sample does not represent an economy-wide result, but this sample seems supportive of Mr. Cordle's analysis. That is, I got less coverage via deductible rates and my employer paid more. I'm very fortunate, my employer has taken the load and preserved my costs (albeit by accepting a higher annual deductible).